ATM Location

ATM Location

Exchange Rate Query

Exchange Rate Query

Featured offers

Featured offers

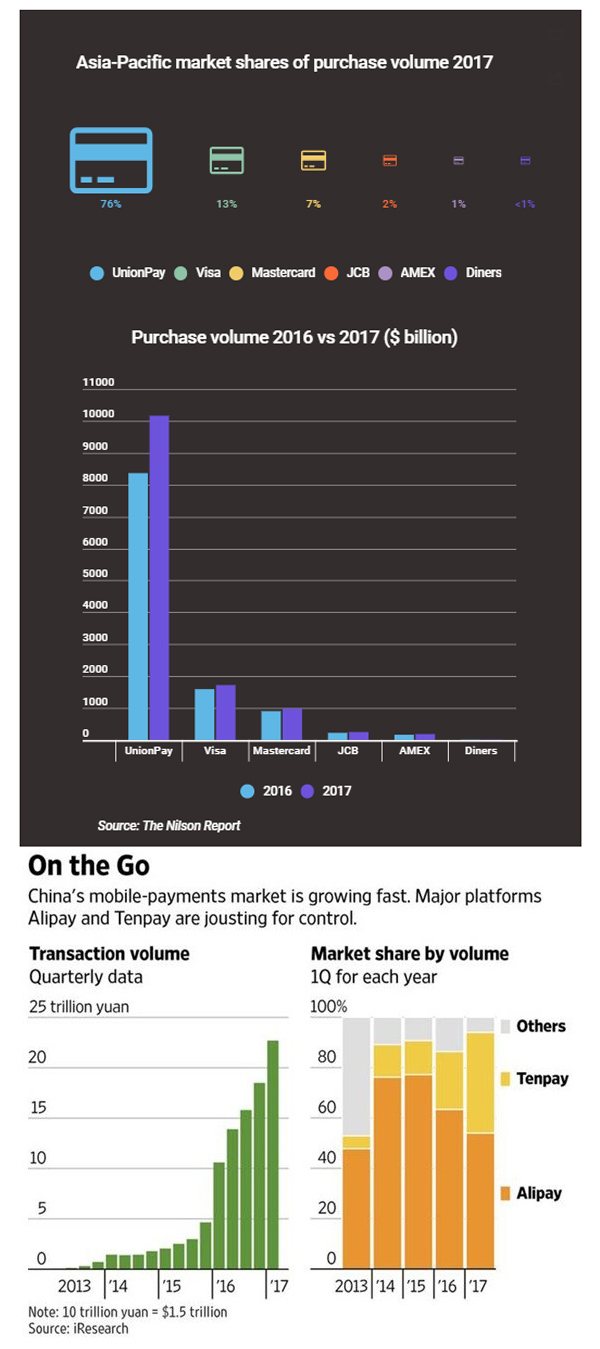

"China Union Pay increased card volumes by 21.3 per cent to $US10.1 trillion in 2017.”

According to data from widely quoted industry monitor Nilson and others, 2017 saw a large increase in card volume across a number of providers: Visa by 8 per cent and Mastercard by 9 per cent while JCB, American Express and Diners Club all increased by over 10 per cent.

However, as impressive as these percentages seem, they are dwarfed by China Union Pay (CUP) which increased its card volumes by 21.3 per cent from $US8.3 trillion in 2016 to $US10.1 trillion in 2017.

When you consider total card volumes in Asia-Pacific are US$13.3 trillion, CUP’s market share is even more impressive at 76 per cent.

CUP’s transactions are predominantly being made in China where Visa and Mastercard have very low transaction volumes. JCB is mostly used in Japan for travel and entertainment (T&E) while American Express and Diners Club are used for T&E across the region.

The payments world in the Asia-Pacific has two main divides – a majority of emerging markets (along with a small number of developed markets) and the broad trends are fundamentally different with very little cross over.

Emerging markets make up 78 per cent of the world population and are heavily dominated by cash. The unbanked population is estimated at two billion or 45 per cent of working adults and many of these markets are in Asia.

Mobile payments, with the exception of China, have limited impact in most Asian emerging markets; although a number of pioneers have developed very efficient and wildly used mobile payments.

China now houses the world’s largest mobile market with AliPay and WeChat dominating the market. India recently launched its own debit card scheme - RuPay - to reduce payment costs and avoid being dependent on Visa or Mastercard.

Different

In developed markets the major themes are very different.

There are a number of strong credit card markets with high cash and cheque use – 72 per cent of global credit card receivables are made in just five countries –Japan, Korea, America, Canada and the UK.

Despite this, China's mobile payment market is still the largest in the world. In 2017, it reached $US3.8 trillion up from $US81 billion in 2012.

Now AliPay has 520 million active users and WeChat has 960 million active users with 40 per cent using the payments capabilities. Between these two platforms, they share 85 per cent of the mobile market and are now threatening the government-owned CUP.

Key to this rapid development and growth is Singles Day, a rebranding of Batchelor’s Day, a 1990s student tradition. Sales for this one day in 2017 totalled $US29.6 billion.

Mobile payments have also expanded overseas to support 100 million travelling Chinese tourists with AliPay available in 28 countries and WeChat in 17.

Chinese mobile payments commonly use QR codes which are not standard at point of sale globally because of concerns about the security of QR codes.

China is by far the biggest e-commerce market in the world.

Consumers spent $US1.1 trillion on online retail channels last year, 32 per cent more than the previous year and more than double the US figure. Rapid growth in mobile payments has supported this growth.

Amazon has found the Chinese market hard to crack so far, mostly because of competition from online retailers like Alibaba and JD.com. Despite more than a decade there, Amazon has less than 2 per cent market share.

Payments are a very high volume, low margin business with even the smallest changes in revenues or margins delivering significant changes in actual dollars. For this reason, Asia-Pacific payment companies face a variety of challenges.

CUP, for all its size and growth, faces internal challenges from AliPay and WeChat - in just four years they are already a third the size of CUP. The international expansion of these players will impact other competitors across Asia-Pacific, notably Visa and Mastercard.

Visa and Mastercard are small players in China and India and this strategic weakness is unlikely to be fixed any time soon. At the same time, they will need to defend their current market share across other markets.

JCB has the size and scale needed to compete, provided it can partner with other global players while American Express and Diners Club are niche T&E players with smaller volumes across the region.

Cost

The cost of retail payment systems is also a major impost on economies - estimated at 1.15 per cent of gross domestic product across Asia-Pacific.

The European Union and World Bank along with associate agencies have undertaken a comprehensive review of payments, considerable policy consultation and targeted research.

A key conclusion of all this work is completion is a key factor in creating successful payments markets.

The key catalyst for change in the payments industry will come from competition. It must be encouraged in all aspects, for consumers, businesses and institutions.

Competition is the seed to foster innovation, it drives change, lowers costs and forces decision making.

It is the most important spark in creating a better deal for consumers and businesses.

Grant Halverson is CEO of McLean Roche Consulting. He has experience as a CEO in financial services and financial technology and has been an investor in fintech.